Questions About the Washington Loan Brokerage Agreement (Cx19136)

Apr 30, 2021

By: Timothy A. Raty; Sr. Regulatory Compliance Specialist

While rules regarding the rounding of numbers on the Loan Estimate and Closing Disclosure have been promulgated, criticized, and debated ad nauseum, rounding rules are almost never promulgated for other disclosures or calculations which are required by law – including the aggregate escrow account analysis required under Federal Regulation X (12 C.F.R. § 1024.17). The lack of such rules for this has caused compliance headaches for lenders and servicers (along with the natural side effects of fines and legal expenses), who must weigh the demands of reality against the demands of the law.

To illustrate a common problem, here is a modified version of Example I in 12 C.F.R. Pt. 1024, App. E:

Disbursements:

$643 for school taxes disbursed on September 20

$4,000 for county property taxes: $2,000

disbursed on July 25 and again on December 10

Cushion: One-sixth of estimated annual disbursements

Settlement: May 15

First Payment: July 1

When an aggregate escrow account analysis is conducted, it involves (in part) the computation of the amounts collected for escrow account items over an escrow account computation year, with the assumption that “the borrower will make monthly payments equal to one-twelfth of the estimated total annual escrow account disbursements.” (Ibid. § 1024.17[d][2][i][A]). This is the “trial balance.” The analysis also includes adding “to the first monthly balance [of the trial balance] an amount just sufficient to bring the lowest monthly trial balance to zero, and adjusts all other monthly balances accordingly.” (Ibid. § 1024.17[d][2][i][B]). A permissible cushion may also be added (see Ibid. § 1024.17[d][2][i][C]) and the aggregate adjustment is then added to the lowest monthly balance of the trial balance, so that it equals no more than “one-sixth of the estimated total annual escrow account disbursements” (Ibid. § 1024.17[d][2][ii]).

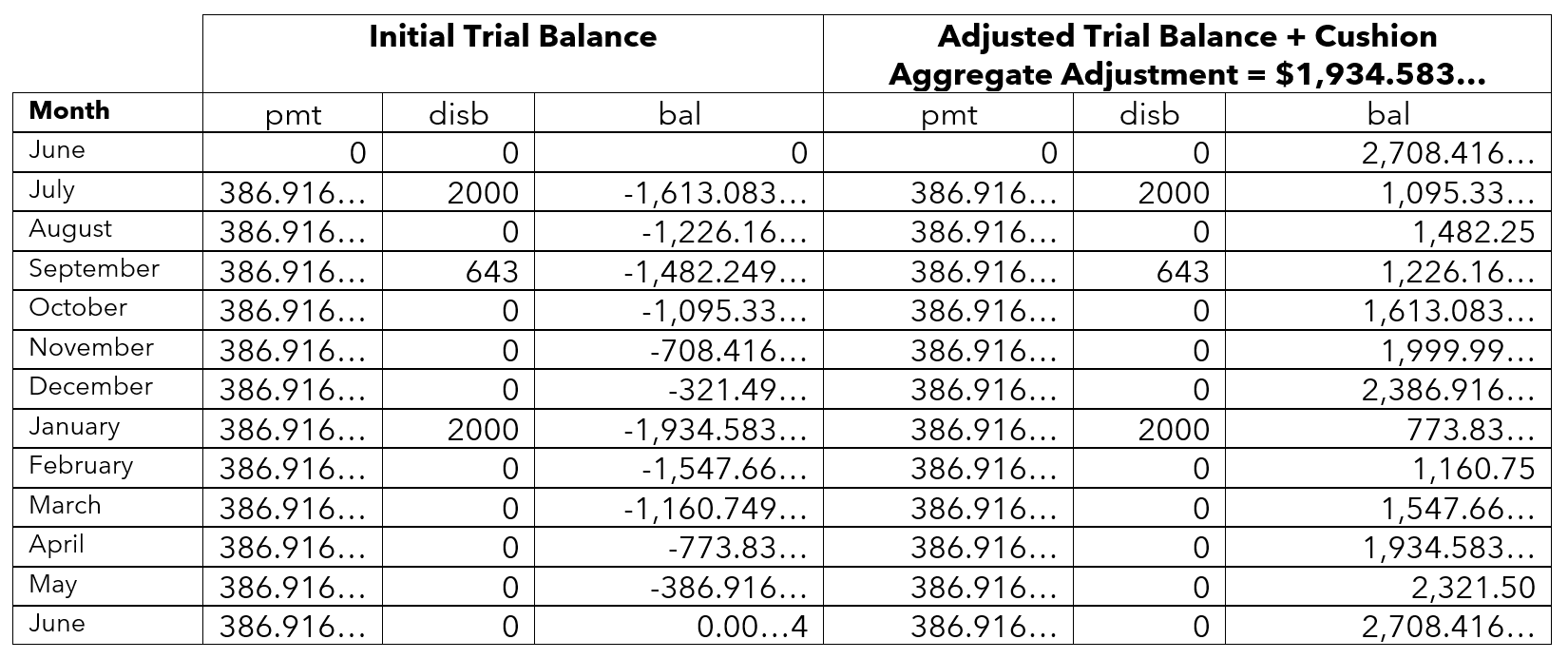

When these calculations are applied to the example above, the resulting amounts are of infinite decimal places (partial cents). One-twelfth of the estimated total annual escrow account disbursements equals $386.9166… and the cushion would equal $773.833… Using these numbers, the trial balances would be as follows for the first two stages of the analysis (with “…” indicating continuing digits):

Naturally, partial cents cannot be collected; a servicer must collect payments in whole cents. Thus, the amounts referenced above must be either rounded or truncated. However, due to the near non-existence of regulatory requirements or guidance on this matter, there is ambiguity as to which method to use and when.

For example, should a lender or servicer truncate the trial balance monthly disbursement estimate of $386.9166… to $386.91? Should it be rounded up from the third decimal place to $386.92? Should either be done before the trial balance is calculated (substituting the “pmt” numbers in the above table with one of these two values) or afterwards (rounding or truncating the “bal” numbers)? These different methods can cause the amounts disclosed and collected to vary from a few cents to a few dollars from each other.

While there is some guidance which does exist, it is not only old, but also contradictory. When the aggregate escrow account analysis rules were finalized in 1994 and 1995, the Department of Housing and Urban Development published in the Federal Register inquiries they received on the new rules, as well as their responses to such, in a “Q&A” format. One of the “Q&As” promulgated the following:

“(a.) May dollar amounts under this rule be rounded?

Answer: Yes, any dollar amount referenced in this rule may be rounded up or down to the nearest dollar.” (60 FR 8812 [1995])

Seemingly, this answer should resolve the issue: If a lender or servicer rounds the amounts used in the aggregate escrow account analysis either up or down to the nearest dollar (at their discretion), then the calculations should be compliant with 12 C.F.R. § 1024.17 (all other things being compliant as well).

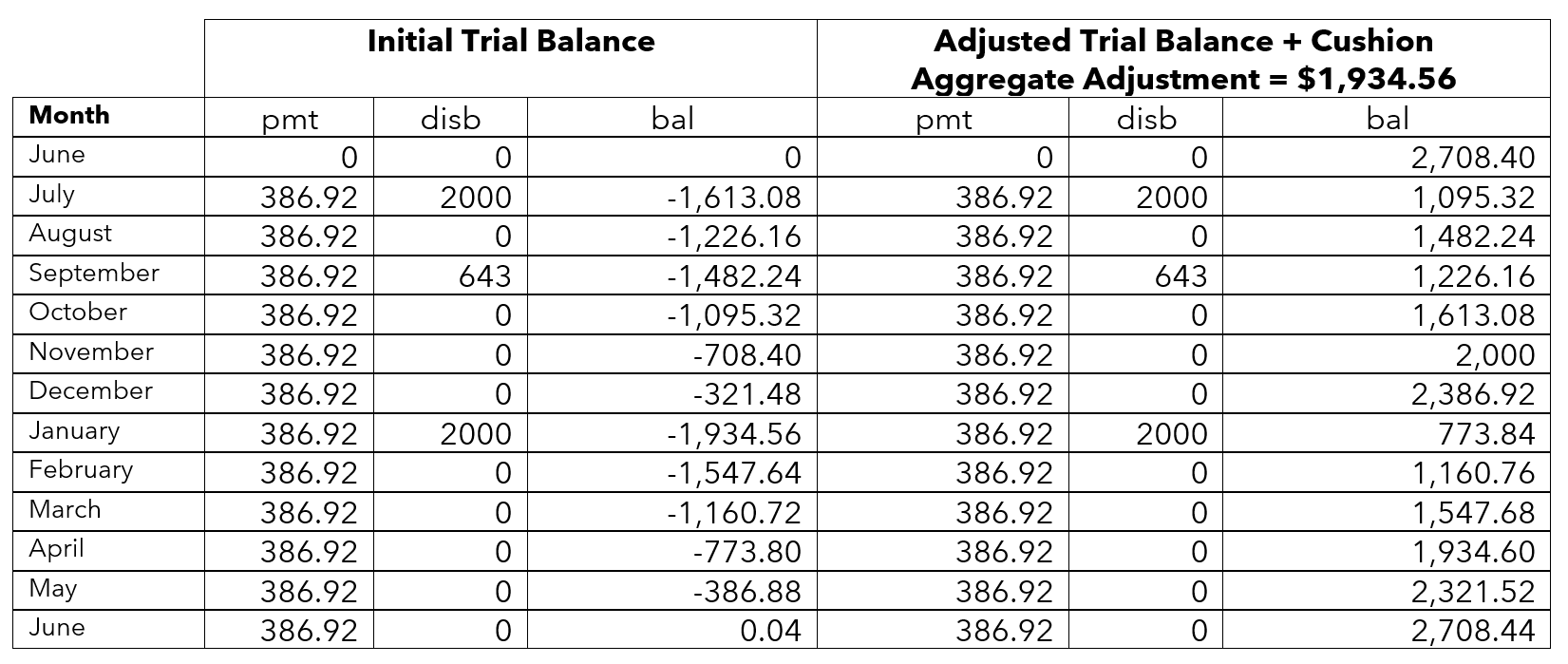

However, issues can arise if amounts are rounded up to the nearest cent or dollar, since doing so will cause technical violations of Regulation X. Using the example above, if the trial monthly amount of $386.9166… is rounded up to the nearest cent ($386.92) and the cushion amount of $773.833… is also rounded up to the nearest cent ($773.84), both before the trial monthly balances are calculated, the calculations will be as follows:

As a result, the servicer will be collecting approximately three-tenth of a cent more per month in the base payment than what the actual one-twelfth estimate of $386.9166… is (for a yearly total of approximately $0.04), along with seven-tenths of a cent more for the cushion, as well as approximately 2.3 cents more in the aggregate adjustment – for a grand total overcharge of approximately $0.07.

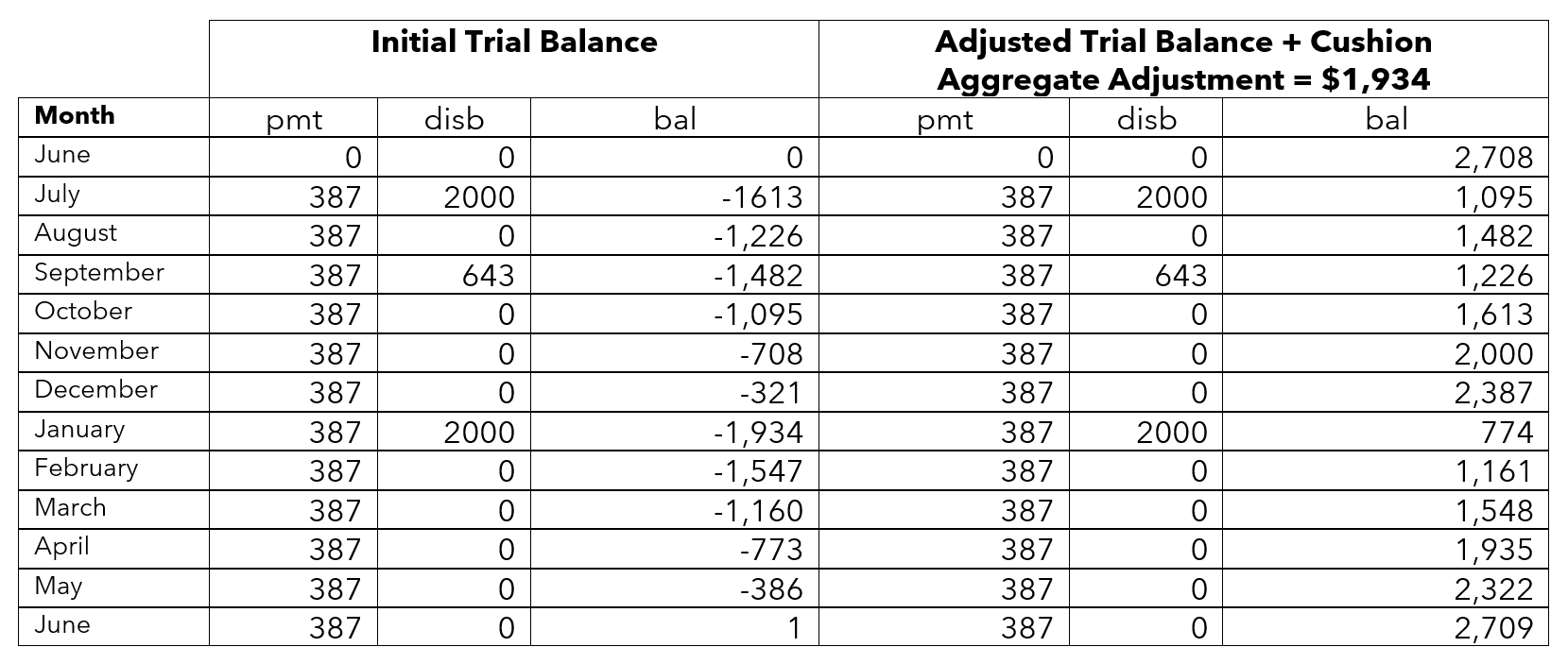

While hardly a monstrous fleecing of the borrower, if HUD’s prior guidance is ignored, such an overcharge is a technical violation of the maximum monthly payment and cushion amounts set forth in 12 C.F.R. § 1024.17(c)(1). It is even worse if the actual estimated amounts are rounded up to the nearest dollar:

Under this scenario, total violations equal approximately 8 extra cents per month ($0.96 annually) with the base monthly payment and approximately 17 extra cents for the cushion – though the borrower will recuperate some of this gouging by approximately $0.58, due to a discounted aggregate adjustment.

While HUD’s guidance would normally alleviate all of these issues, it was directly contradicted by the Federal Reserve Board in an article they published in the Second Quarter issue of their Consumer Compliance Outlook in 2009. This article outlined common escrow compliance issues the FRB found in their exams, including the following:

“Overcharges in the collection of initial escrow deposits generally result when errors are made in the initial analysis. Other calculation or system entry errors can result in errors in the escrow deposit amounts. Some examples include: . . . Rounding adjustments to create an even dollar amount.” (p. 6)

In addition to this, HUD’s guidance applied to their version of Regulation X (24 C.F.R. § 3500.17) which was repealed in 2014, several years after its provisions were practically transferred to 12 C.F.R. § 1024.17 and placed under the enforcement of the CFPB. To this date, the CFPB has not issued any formal guidance on this matter and it is dubious as to what extent either HUD’s or the FRB’s previous guides still apply.

Also, while both HUD’s and the FRB’s guides may still apply to Federal Regulation X, they certainly do not apply to State laws which also restrict the amounts which may be paid into an escrow account.[i] Whether rounding or truncating is permitted (and how) under these laws is up to State authorities.

Altogether, there is enough ambiguity to raise serious questions as to what extent lenders and servicers can use rounding or truncation methods in developing the disclosures required under Ibid. § 1024.17(g) through (j), as well as in determining the exact amount of monies they may collect from the borrower. Until the CFPB and/or State authorities provide further guidance on this matter, it will remain ambiguous.

Special Thanks to Windows 10 Scientific Calculator for its assistance in writing this article.

_____________________________________

[i] E.g., see Ariz. Admin. Code R20-4-1811; Idaho Code Ann. § 26-31-212(2); Neb. Rev. Stat. § 45-101.05; Mont. Code Ann. §§ 71-1-113 & 71-1-114; and Vt. Stat. Ann. tit. 8, § 10404

The preceding is for informational purposes only and is not and may not be construed as legal advice. No third-party entity may rely upon anything contained herein when making legal and/or other determinations regarding its practices, and such third party should consult with an attorney prior to embarking upon any specific course of action.